CHINA AT THE CENTER OF ATTENTION

By Alexandre Hezez, Group Strategist

Editorial

In its latest annual report, the IMF highlights the historic period we are living in around the world. The first sentence written by Kristalina Georgieva, its director general, is significant: “The world economy is going through the greatest test it has seen since the Second World War “. In her wishes, she predicts a“more difficult” year in 2023 for the world economy, against the backdrop of a slowdown in the main growth engines.

The pandemic is certainly still ongoing. And just as we were seeing the first signs of economic recovery, the world was faced with a second unprecedented shock: Russia’s invasion of Ukraine. Soaring food and energy prices and widespread inflation are hitting from all sides with an accumulation of risks.

But at the beginning of this year, it is China that is at the center of all the attention. The contraction of activity in the country has worsened as a result of the epidemic. The official PMI indices for December show the extreme disruption caused by the wave of Covid-19 infections that is still affecting the country. Despite the abandonment of the “zero-covid” strategy and the reopening of the Chinese economy since the beginning of December, the services sector is penalized by the weakness of Chinese household consumption. The latter voluntarily limit their travel for fear of contracting the virus. The manufacturing sector is also not spared and continues to contract. These levels suggest a sharp contraction in GDP for the4th quarter. Beyond the December low, the average PMI for the entire quarter is approaching the levels of the1st quarter of 2020 in services.

Source : Bloomberg

The implementation of a new health policy now seems to be a given from a social, economic and political point of view. According to Xi Jinping, China has shifted from the ” zero Covid ” strategy to the ” control Covid ” strategy.

However, we believe that as the current wave recedes, economic growth should rebound significantly throughout 2023. As evidence, economic activity is rebounding in several Chinese cities where Covid infection has likely already peaked, although many parts of the country are still struggling with skyrocketing cases and mobility is still well below levels reached a few months ago.

China is expected to grow slowly in the first half of the year, with the reopening initially triggering an increase in Covid cases and delaying the return of household consumption, but it should accelerate sharply in the second half.

and industrial production

Source : Bloomberg

More government support could help consumption become a key pillar of economic growth in China this year.

Proposed measures to stimulate consumption include extending tax exemptions for green energy vehicles, increasing the use of consumer vouchers, increasing government tax transfers to households, optimizing epidemic controls to support the food and restaurant sector, and building confidence in the real estate sector. Following the disruption caused by Covid, better policy coordination is needed in social security, consumer finance, rural revitalization and income distribution.

In this respect, the Chinese Ministry of Finance declared a few days ago that new budgetary measures would be taken in order to promote growth in 2023, in particular by supporting the finances of local authorities or by introducing tax relief for companies.

At the geopolitical level, the G20 in November contributed to the decrease in international tensions with the meeting between Xi Jinping and Joe Biden, which was the first official meeting between the countries since Nancy Pelosi’s visit to Taiwan in August. The appointment of the former Chinese ambassador to the United States as foreign minister is yet another element in the easing of tensions between the two countries.

At the monetary level, the PBoC (Central Bank of China) will remain a support. The latter has pledged to support domestic demand and maintain “efficient” credit growth as the economy reopens after the restrictions. Monetary policy “will focus on stabilizing growth, employment, and prices, as well as supporting the expansion of domestic demand.”The People’s Bank of China said in a statement after the quarterly meeting of the monetary policy committee, which was convened by Governor Yi Gang.

Sources: Bloomberg, Richelieu Group

China’s economic and sanitary health is obviously not without consequences for other geographical areas due to the impact of a decrease in constraints in the supply chain. Chinese growth should therefore rebound in 2023 to 4.8% from 3% in 2022 and be the main driver of global growth in 2023. The lifting of the Covid zero policy and support for the economy, especially the property market, will revive Chinese credit and consumption. This will have positive consequences in terms of demand for foreign products.

The question will be to monitor the impact this will have on global inflation. Many analysts believe that the risk will be additional upward pressure on prices given the Chinese economic recovery. Commodities could be on the rise again, as evidenced by iron prices. Indeed, the price of iron depends mainly on China, whose steel mills buy more than two-thirds of the world’s volumes.

Source: Bloomberg

Conversely, a China that remains mired in its health policy would lead to even more painful stagflation. Certainly the explosion of cases on the spot is increasingly worrying, many countries are taking restrictive measures against travelers coming from China. But knowledge of the virus, testing processes, and behaviors have nothing to do with February 2020. The next few weeks will bring their share of doubts.

We believe that the reopening of China will accelerate the rebalancing of the economy and trade through the mitigation of supply chain disruptions and will therefore have a positive impact, both in terms of growth and disinflation in 2023.

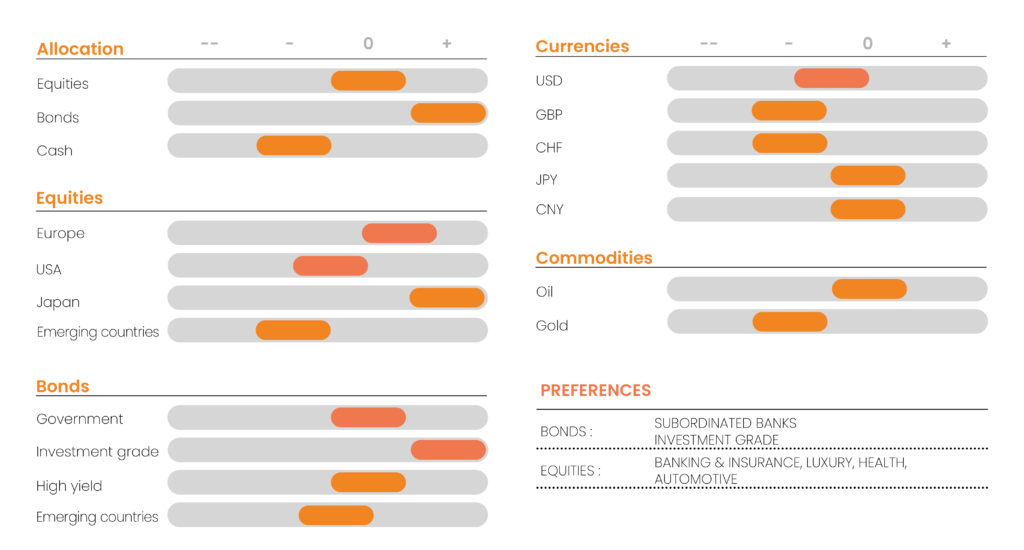

CONVICTIONS

POSITIONING WITH RESPECT TO RISK CRITERIA

As we reported last month, paradoxically, 2022 has been marked by good resilience in corporate earnings. 2023 will be much more complicated.

The reopening of China is the focal point to watch in the coming weeks. For the moment, the spirit is one of distrust on the part of the authorities of other countries, but we continue to believe that this reopening will have a positive impact on the year.

We indicated that the month of December presented some risks, particularly concerning the central bank meetings. This was indeed the case and Equity indices corrected widely between -3% and -10% in local currency.

Central banks are determined not to remain trapped in the inflation trap. Christine Lagarde did not hesitate, during her press conference, to assure that several key rate hikes described as “rapid and significant “were still to come, specifying that the step would be 50 bp. Federal Reserve Chairman Jerome Powell has sought to convince investors that interest rates will head to a level above 5% in 2023 and stay there until high inflation is brought under control.

We believe that the pivotal rates will be reached in the second quarter, which will finally give investors more visibility. Central bank rates should remain at their level for a period of several months allowing inflation expectations to steadily decline. In the meantime, the market can be scared off by the release of economic figures.

We believe that investors will be looking for yield at the beginning of the year, whether it be in the form of equity dividends or bond coupons.

In geographical terms, the very mild winter in Europe and the scheduled reopening of the Chinese market should be favourable to European companies. However, we remain circumspect about the ECB’s aggressive, even overly aggressive, attitude. The financial sector (banks and insurance companies) continues to be favored under these conditions. Companies linked to the end of zero Covid and Chinese pro-cyclical measures are to be favored (luxury, consumer discretionary). Japan will benefit from the reopening of the Chinese economy and stronger growth, linked to a catch-up effect. For now, we prefer to bet on China’s reopening in an indirect way. The mild winter is likely to reduce the risk premium on the industrial sector, given the distance from the blackout.

As for emerging markets, we continue to think that we need to wait for the Fed’s pivot and that it may still be a bit early to reinvest heavily, even if the prospect of a weaker dollar improves visibility. We believe that in the first quarter the bond sector is the preferred sector, as rate hike expectations are largely driven by central bank action. Flows into bonds will increase as disinflation takes hold. If further short-term rate hikes appear until the second quarter, a potential change in direction by central banks will be beneficial. Although it is difficult to predict with certainty the point at which monetary policies will change, it seems relevant to consider the opportunities offered by this asset class. In December, volatility and lack of liquidity impacted the segment but we believe spreads should tighten during 2023 by about 100 bps adding capital gain to the current yield.

For the time being, we prefer investment grade and high yield (BB+). At the same time, we are increasing the duration of the portfolios to take into account lower inflation expectations and growth potential for 2023.

Given the deceleration in global growth and the expected decline in earnings in the first half of 2023, they should outperform.

We remain positive on the overall bond segment. Bonds ” crossover ” are still particularly interesting. The headwinds are expected to diminish during 2023, allowing for an improvement in the business cycle and a gradual increase in risk exposure in the portfolios. We favor companies with strong balance sheets and high cash generation. A scenario of a moderate recession should benefit the bond segment over 2023, which could be a mirror image of 2022. The riskiest segments are still to be avoided as refinancing difficulties and operational impacts are only just beginning. Uncertainty about the Fed and higher-than-expected inflation were the main drivers of wider spreads in 2022. On the other hand, the decline in Fed-related uncertainties should allow IG spreads to tighten despite somewhat weaker credit fundamentals next year.

MACROECONOMIC POINT

The turnaround in US real estate is confirmed

Real estate sales are down 35% year-over-year, and price increases are slowing significantly. According to the NAR, U.S. sales commitments have plunged nearly 38% in one year. A drop largely due to the pace of increase in real estate interest rates the fastest ever recorded. The number of promise-to-buy signatures has fallen sharply. The housing market has seen the most visible effects of the Fed’s aggressive interest rate hikes, which are intended to curb high inflation by weighing on demand. The 30-year mortgage rate rose above 7% in October for the first time since 2002, more than doubling in the space of nine months. This will put a damper on a housing market that has been buoyed in recent years by historically low borrowing costs and a rush to the suburbs during the Covid-19 pandemic. Redfin noted that the median price rose “only” 2.6 percent year-over-year, its slowest pace since May 2020. House prices continued to fall in October, lowering the annual rate of increase (Case-Shiller index at +8.6% year-on-year), a sign that the transmission of monetary policy to the housing market will take several more months.

Sources : Bloomberg & Richelieu Gestion

Central banks will be watching for signs of monetary tightening effectiveness in 2023

The economic data published at the end of the year sent favorable signals regarding the effectiveness of central banks’ monetary tightening. Thereis still a long way to go and this will encourage central banks to maintain a permanently restrictive monetary policy in 2023 or even 2024.

In the eurozone, the ECB’s tightening of financial conditions is beginning to bear fruit, as evidenced by the slowdown in lending to businesses and households. Lending moves in tandem with economic activity and employment, two factors on which the ECB needs a slowdown to ward off fears of an inflation-wage spiral.

The contraction in Spanish retail sales volume is another positive signal for the ECB. In the United States, the persistence of inflationary pressures in the labor market is prompting the Fed to maintain its restrictive stance. Weekly jobless claims are rising but remain at low levels, reflecting continued high pressures for second-round effects (the impact of past inflation on wages). After real estate, employment data in the United States will be closely scrutinized to assess the effectiveness of the Fed’s policy on the labor market. The decline in these pressures will only be gradual, which will also delay the relapse of core inflation towards the 2% target and justify the Fed’s decision not to cut key rates in 2023.

Sources : Bloomberg & Richelieu Gestion

MARKET POINT

EMERGING BONDS : selectivity in sovereigns

Emerging market bonds have not been spared, with declines of 17.6% for dollar-denominated debt and 6% for local currency debt. Valuations are more attractive, sentiment is much better. Fundamentals can change dramatically for the better once rates peak in the U.S. and China reopens its economy. Volatility is expected to remain high, especially in the first quarter, until the Fed’s hikes are finalized.

Debt today offers what we consider to be extremely attractive valuations, providing a significant buffer against rising yields, with emerging market hard currency and local currency debt offering yields around 11-15, the highest in two decades.

The year 2022 will also have been marked by a new surge in restructurings on border markets for countries already weakened by the Covid pandemic, and now by rising rates and the impossibility of accessing capital markets. In the last two years, a dozen defaults have been pronounced, including those in Ghana recently, in addition to those in Sri Lanka and Ecuador this year. Emerging countries with strong fundamentals should attract capital flows, which will allow emerging countries to enjoy a better 2023. This implies a weaker dollar, which should also enhance the attractiveness of emerging debt. Central banks will have more freedom to conduct monetary policy under fewer constraints. The EMBI Global Diversified spread will widen to about 500 basis points, but the significant rise in yields this year should allow performance to return to positive territory.

The IMF expects energy exporters in the Middle East and Central Asia to earn a cumulative revenue of about $1, 000 billion between 2022 and 2026. The GCC, which has good relations with the West and Russia, is energy independent and is undergoing many social reforms. The average current account surplus of the Gulf countries is expected to be close to 10 percent of GDP in 2022, almost double the level of the previous year, and is projected to reach 7.8% in 2023.

In contrast to 2022, when debt ratios generally declined in Latin America due to high growth rates, the outlook is more mixed for 2023. Debt ratios are expected to increase more in Brazil (+5.1%) and Chile (+2.7%) and decrease in Costa Rica (-1.9%) and Ecuador (-1.8%). The political risk remains high in Brazil. On Colombia, it is very likely that the positive catalysts will materialize : abandonment of the ban on new oil exploration contracts (the President will increase taxes on this industry), recovery of part of the revenue from the 2022 tax reform and reduction of land purchases.

Source : Bloomberg

EMERGING EQUITIES: Maybe still too early ?

Emerging equities suffered heavy losses in 2022, driven by a combination of monetary tightening, a stronger U.S. dollar, a general economic slowdown, and the aftermath of the Russian invasion of Ukraine.

The proactivity of emerging market central banks, which reacted very quickly in 2021, combined with inflation near its peak, could facilitate a rebound in emerging market assets in 2023.

A change in sentiment and growth dynamics is necessary and must materialize.

China is a potential source of growth in 2023. Valuations remain attractive, but we believe the main support lies in the Fed’s tightening peak. After the Fed’s pivot, we expect emerging assets to rebound. This is when emerging assets perform best historically.

For equity markets, with valuations generally below historical averages (except for India), the catalysts of the end of the Zero-covid policy and the Fed’s pivot will soon be met.

The inflation outlook in the U.S. is the central element to consider in the trajectory of emerging equities. The positive impact of the Fed’s pivot will only be felt in the second half of 2023. We maintain a cautious stance as we enter the first phase of 2023.

Sources : Bloomberg & Richelieu Gestion

Synthesis Strategy Richelieu Group – Author

Disclaimer

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

This document was produced by Richelieu Gestion, a management company and subsidiary of Compagnie Financière Richelieu. This document may be based on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is reliable and complete. The opinions, views and other information contained in this document are subject to change without notice.

The information, opinions and estimates contained in this document are for information purposes only. No element can be considered as an investment advice or a recommendation, a canvassing, a solicitation, an invitation or an offer to sell or to subscribe to the securities or financial instruments mentioned. The information provided concerning the performance of a security or financial instrument always refers to the past. Past performance of securities or financial instruments is not a reliable indicator of future performance.

All potential investors should conduct their own analysis of the legal, tax, accounting and regulatory aspects of each transaction, if necessary with the advice of their usual advisors, in order to be able to determine the benefits and risks of the transaction and its appropriateness to their particular financial situation. He does not rely on Richelieu Gestion for this.

Finally, the content of the research or analysis documents or their excerpts, if any, attached or quoted, may have been altered, modified or summarized. This document has not been prepared in accordance with the regulatory provisions designed to promote the independence of financial analysis. Richelieu Gestion is not prohibited from trading in the securities or financial instruments mentioned in this document prior to its publication.

Market data is from Bloomberg sources.