Mid-Term : A 2022 election like no other

By Alexandre Hezez, Group Strategist

Editorial

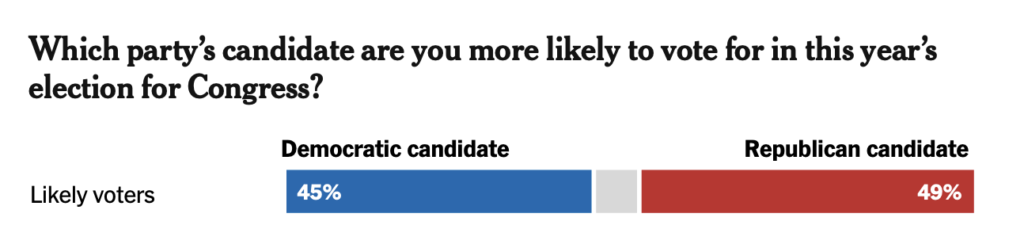

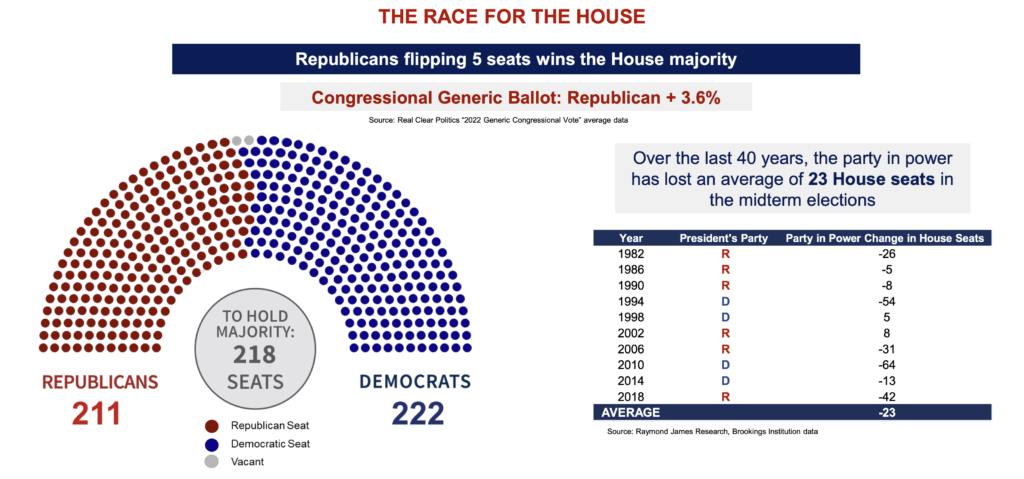

The majority of political experts believe that Republicans are likely to win a majority in the House of Representatives, but control of the Senate is less certain. Republicans enter the final week of the race for control of Congress with a narrow but distinctive advantage. The economy and inflation have become the highest concerns, giving the Republican Party the momentum it needs to take back power from the Democrats. According to a New York Times/Sienna College poll, 49% of likely voters said they plan to vote for a Republican to represent them in Congress on November 8, compared to 45% who would vote for a Democrat. This result marks a marked improvement in favor of Republicans since September.

Recent history has shown that many things can change between now and the election. The energy issue is central and we may see decisions by the current presidency on the use of oil stocks or export limits on gasoline to positively impact the purchasing power of American households and reverse the recent trend. Democrats may retain both houses, but usually the party in power loses seats. When the Republicans held both houses in the 2002 mid-term elections, Bush maintained his policies and accelerated the implementation of his previous tax cut. The situation is completely different in 2022.

A Democratic victory would reinforce current policy: more spending on the child tax credit, renewable energy and Medicaid with tax increases, and more opposition to fossil fuels. This could, if anything, raise doubts about inflation expectations and an even more restrictive central bank to combat rising prices.

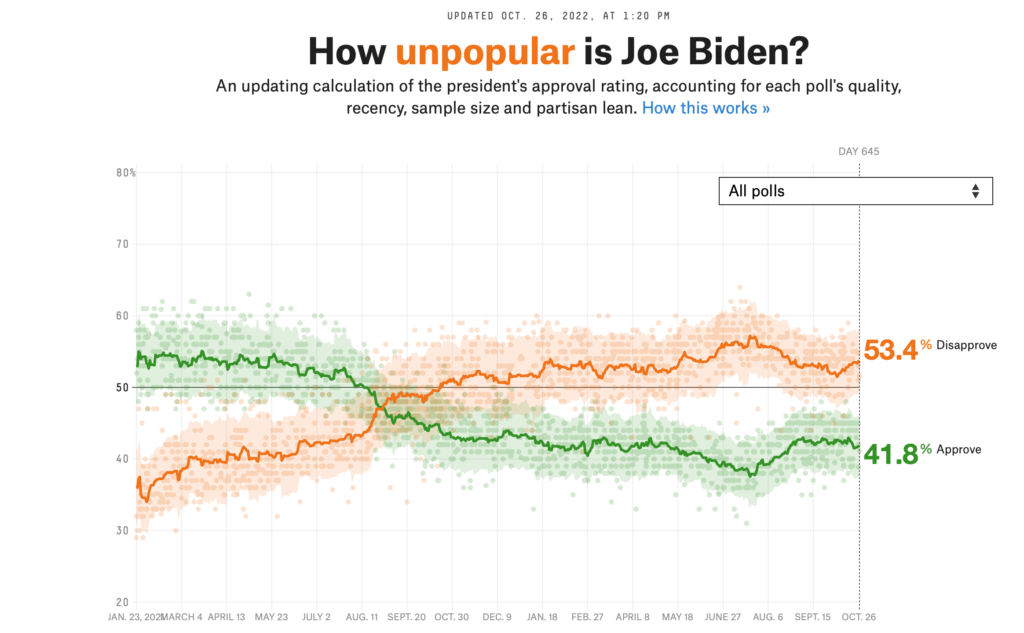

This election comes at a time when Joe Biden’s approval rating has plummeted since his election. His low approval rating is primarily due to the highest inflation levels in the country in four decades. The midterm elections could see the Republicans make further gains and thrive on the dissatisfaction with the incumbent government, as always.

Some states are particularly scrutinized. Pennsylvania, a key swing state in the mid-term elections, is swinging from one trend to another, with its large cities more in favor of the Democrats and its rural areas more pro-Republican. Texas, too, where the issues of abortion and immigration dominate and captivate the debate with an ever present Donald Trump.

In some ways, this election is more like a presidential election than a mid-term election. Normally, these elections do not cause much variation; they usually serve as a referendum on the incumbent president. However, a series of conservative-majority Supreme Court decisions (on abortion, guns, the environment, education, and other issues) has shifted the balance of power. Biden’s victories (including the passage of his climate, tax and health care bills) and Donald Trump’s return to prominence (with the revelations of the Capitol Hill assault investigation) should have changed the dynamic. However, polls show that voters are prioritizing the economy over threats to democracy. They are more concerned about immigration than abortion.

This is bad news for Democrats. Polls show that the party has all but lost the House of Representatives. Republican control of the lower house of Congress would be enough for the party to challenge the Biden administration.

“Americans shouldn’t have to choose between driving to work and putting food on the table. Republicans are committed to restoring America’s energy independence and lowering gas prices.”

Kevin McCarthy , Republican Leader in the House of Representatives

Economic factors are refocusing voters on inflation and high fuel costs in the home stretch, leading us to believe that a Republican victory is the most likely outcome.

The environmental issue is another significant effect of the election results. Republicans will consider Joe Biden’s agenda: the Inflation Reduction Act and energy transition modeling ($737 billion, including $369 billion for climate and energy investments). It should be noted that no Republicans voted for the passage of this legislation. This could play a crucial role in its implementation by disrupting the actual execution. Voters will therefore determine the fate of the climate and energy program, which remains highly controversial.

Spending is not the only grievance Republicans have with the Biden administration’s climate and energy policies. The Inflation Reduction Act remains highly controversial. It provides funding for several key facets of the Biden administration’s climate and energy agenda, potentially enabling the country to meet the President’s goal of reducing emissions by at least 50 percent from 2005 levels by 2030. A key factor in achieving this goal is to deploy more renewable energy, which requires a significant investment. The long-term tax credits in the legislation could catalyze private investment in renewable energy, which is already booming. If the U.S. is to fully meet its emissions reduction goals, it must build its electric workforce and transmission capacity, as well as strengthen-and for products such as battery metals-create resilient supply chains.

The potential impact of the Midterms on the equity markets

In terms of stock market performance, midterm election years are not like other years. The second year of a presidential term follows a predictable pattern: average stock returns tend to fall in the second and third quarters, with high market volatility, followed by a stock market rebound at the end of the year and in the first half of the following year.

after the mid-term elections since 1946

Source : Bloomberg, Richelieu Group

Financial Markets: Since 2004, the S&P 500 Index returns have been below average in the 60 days prior to the U.S. elections. The mid-term elections were more mixed in the two months following the election.

This year remains, in many ways, unfortunately exceptional. The performance of the S&P 500 in the 2 months leading up to the midterm elections is very negative (so far), the worst performance since 1946 (no midterm election year comes close to this poor performance). This mid-term election period will be unique and statistical analysis can be hazardous.

While 12-month forward returns have been strong even when equity markets were down prior to the mid-term elections, the shorter-term return profile after the elections may be negative.

At this point, with the market now focused on inflation, Ukraine and U.S.-China tensions, equity markets have yet to factor in the potential impacts of the midterm elections.

The most favorable outcome for the markets would be a Republican victory in the House and Senate. If the Republicans take the House and not the Senate, that would also be a relatively favorable outcome. Democratic presidents have an advantage in terms of market performance. From 1945 to the end of 2021, the S&P 500 has returned 9.4% under Democratic presidents, compared to 6.6% under Republican presidents. The best returns occurred under Democratic presidents held in check by a Republican or split Congress. Generally, investors prefer divided power in the federal government. Indeed, a divided or Republican Congress would likely not pass any major legislation by the next presidential election and with the U.S. economy in good shape, this scenario would be popular with investors. We believe that this election will have an impact on the financial markets, particularly in the perception of inflation and its impact on the economy.

Investors should be sensitive to potential fluctuations in stocks and bonds during mid-term election years, but should remain calm to avoid making decisions at a time of heightened volatility.

The only real uncertainties remain inflation and the Fed’s ability to control it without “killing” current growth. Despite the higher than expected numbers, we continue to believe that clearer signs of disinflation in the U.S. will emerge by the end of the year. Beyond the political aspects, it is U.S. inflation that will shape the future trend of the overall market.

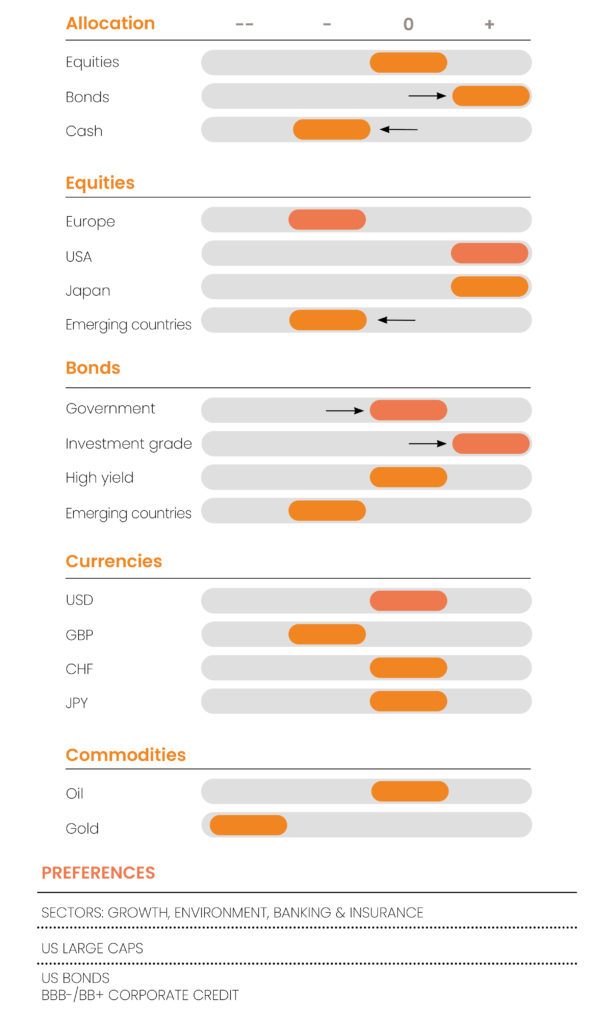

CONVICTIONS

POSITIONING WITH RESPECT TO RISK CRITERIA

Weeks go by and they look the same…. Well, not quite the same! Governments and central banks are caught between the hammer of inflation and the brick wall of recession. The Liz Truss episode in the UK has shown that fiscal policies must be targeted and non-inflationary. We believe that European governments will not make this mistake. Central bank rate hikes are starting to have their recessionary effect as the latest leading indicators show.

Our macroeconomic scenario is a sharp recession and inflation that persists at levels that are unsustainable for European monetary authorities. Rates are likely to rise again rapidly. The ECB refinancing rate is expected to reach 2.5%. The reciprocal attitude between the European states and the new Italian government demonstrates Europe’s willingness not to disunite despite the tensions; this should support the euro against the dollar at parity. Our target for 10-year sovereign rates at the end of the year is 2.50%, 3.00% and 4.50% for Germany, France and Italy respectively. The growth outlook is also weak in the US, although there are some positive signs that the US economy is resilient and, above all, that the FED is determined not to plunge into recession. US real estate is expected to fall by 10% in the coming months and will drive the shelter component of the inflation numbers down. The latest real estate data confirms this belief that we have had for a few months. The recent dovish comments by Fed members, who insisted on the risk of too much tightening of financial conditions, and publications that, for the moment, are reassuring investors who were expecting much worse, are leading to a more temporary serenity. The mid-term elections should provide greater political visibility over the next two years.

In terms of bonds

The sharp corrections in the bond markets have brought yields to their highest levels in a decade and we believe this opens up an interesting opportunity in the overall bond market as some central bankers begin to anticipate a stabilization of monetary policies in Q2 2023. On the sovereign side, we favor the US side. The Fed is expected to pause in Q1 2023 and anchor its policy rate at 4.75%. Given the economic growth, the yield curve will remain slightly inverted and will allow the 10-year rate to remain at around 4.5% (with inflation expectations stabilizing). In the Eurozone, we remain cautious on sovereigns and constructive on corporate credit.

The crossover part (BBB-/BB+) is particularly interesting even if we could still see some volatility. Default rates will certainly rise but forward yields over a 4/5 year horizon are particularly attractive (5.5%/6%). In this context, stock selection will be particularly decisive. Attractive opportunities are beginning to present themselves for investors in the credit areas where spreads have widened considerably without any real discernment.

Sources : Bloomberg & Richelieu Gestion

On the equity front

It seems clear that corporate profits will be affected by the weak economy as rising input costs impact margins and financing conditions have deteriorated. However, apart from the fundamentals that continue to deteriorate, we believe that the market balance is conducive to market rallies at the end of the year, which will have to be justified by reassuring inflation publications. Note that hedging positions, cash at historic levels in funds and index volatilities remain very high and the slightest good news could lead to violent self-fuelling reversals. We are maintaining our neutral positioning on equities with a more positive view in the very short term. We continue to believe that US equities are more likely to rebound because the FED has the keys to balancing growth and inflation. This is not the case in Europe, where exogenous risks make monetary and fiscal policies subject to geopolitical and climatic risks. These same risks could obviously turn into opportunities.

In Asia, the BoJ, by maintaining its accommodating policy, should support Japanese equities in local currency. China is a concern with respect to Xi Jinping’s political and geopolitical ambitions. The positive “Communist Party Congress” effect did not take place. The yuan fails to stabilize. The “Zero Covid” policy could be maintained and the relations between China and the United States will remain uncertain, which leads us to put an additional risk premium on the zone. We are cautious on the country.

In terms of themes

A few sectors that will come out on top: the environment across the entire value chain (from production to the energy efficiency of buildings) with the colossal investments needed in the future, and the luxury sector, which is benefiting from a catch-up in consumption in Asia and pricing power that remains more than appropriate in the current environment. The initial results of financial companies in the US are reassuring and show that the impact of the rise in interest rates will be beneficial despite the increase in the cost of risk. On a more speculative basis, the banking and insurance sector should attract investors at the beginning of the year. We believe that banks are a good hedge against a hawkish Fed as they benefit from a higher NIM (net interest margin). We believe that this effect will be more important than the concern about the risk of lower credit growth. The quarterly results of the US banks have proven this. We are still underweight industrials, especially in Germany, and companies with too much operating leverage (low cash flow) because they will start to suffer from the deterioration of financial conditions. With regards to these companies, we prefer to invest in debt rather than in equities (crossover bonds: BBB-/ BB+). Even if the valuations of small caps are attractive, it is too early to reinvest given the lack of liquidity and deteriorating credit conditions. We continue to believe that quality companies will benefit from their competitive positions. Large technology stocks should regain favor with investors because of their balance sheets, while debt-laden companies remain in an uncomfortable position.

Sources : Bloomberg & Richelieu Gestion

In terms of diversification

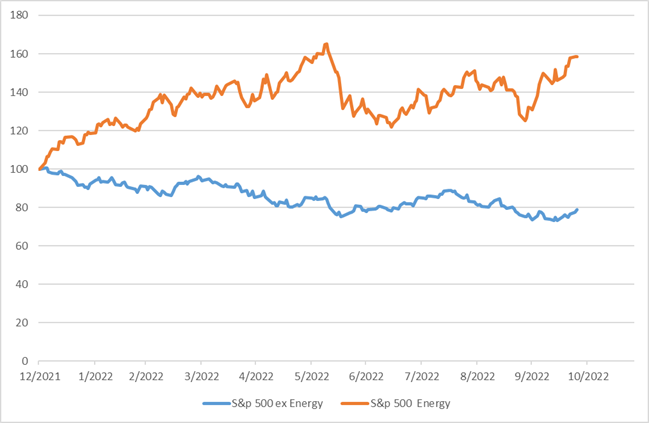

2022 was a particular year in which diversification played little role. The dollar was the only safe haven asset for a “non-US” investor and there was none for a US investor (his reference currency being the US currency). Bonds (of all types) and stocks (except for oil stocks) have fallen significantly. It is therefore likely that the rallies we are experiencing will lead to a re-correlation of the major indexes, as we have experienced. Stock selection will undoubtedly play a major role in the coming months, beyond sectoral or geographical aspects.

Our central scenario

Our central scenario remains that monetary policies will be able to gradually ease in the latter part of the year.Central banks should therefore tighten financial conditions less quickly, and then stop doing so in the first half of 2023, without however going back before 2024, which is likely to keep bond rates at high levels. Slower growth will help inflation to fall back, allowing monetary tightening to slow in the coming months, putting a stop to the upward movement in sovereign rates.

Sources : Bloomberg & Richelieu Gestion

The scenarios that would lead us to position ourselves more strongly in the market are the decline in U.S. employment and housing numbers and, most importantly, a change in Fed rhetoric. We need the monetary tightening cycle to finally be sufficient to bring inflation back into line with the central banks. If not, we remain convinced that central banks will continue to act and keep all risky assets in an uncomfortable position.

MACROECONOMIC REVIEW

The Fed’s desired economic slowdown is underway

The third quarter GDP in the United States confirms the expectations of financial investors as to the need for the Fed to extend the increase in key rates, in a context of continued rise in sovereign rates. The various activity indicators of the past few months have highlighted the marked resilience of activity, mainly at the consumer level.

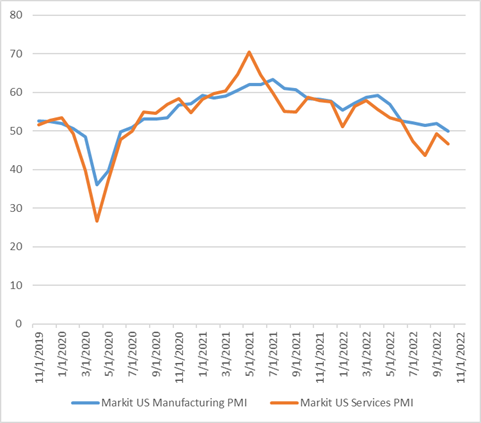

It should be noted that while the ISM manufacturing index continued to fall over the past quarter, services, which account for a large share of US GDP (80%), fell significantly. The Fed’s action is bearing fruit and, paradoxically, this is good news. The Fed wants to cool the economy and ease the labor market, and then get prices under control. A few signals confirm that inflationary pressures and the labor market are beginning to ease, in line with a slowdown in activity.

The housing market continues to slowdown, leading to a sharp sequential decline in home prices according to the August Case-Shiller index that was released. While the impact on the rent component of inflation will be delayed, it is already a positive signal that the Fed is beginning to slow the pace of rate hikes, especially as the rest of the economy continues to slow. A permanently tight monetary policy is still needed, but with 75 bps of rate hikes soon. The Fed will move closer to its target level, in our view 4.75%/5%, and the integration of an upcoming end to the rate hike cycle will be a major reminder to break the upward momentum on long rates. Discussions at the FOMC show some reluctance to go much further. San Francisco Fed President Daly, for example, said on Friday that the Fed must be cautious in its monetary tightening to avoid plunging the U.S. economy into an “unprovoked slowdown. We believe this should, in turn, reduce market volatility.

Sources : Bloomberg & Richelieu Gestion

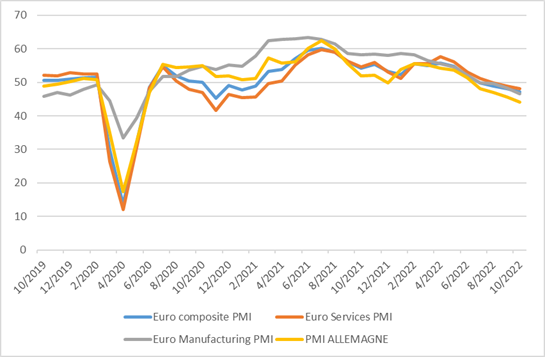

Europe : solidarity is put to the test

Eurozone PMI data for October once again came in below expectations. The manufacturing and services indexes continue to fall, reaching 46.6 and 48.2 respectively. The drop of the composite index below 48 reinforces the hypothesis that the Eurozone will enter a recession as early as the 4th quarter of this year. This result could call into question the ECB’s macroeconomic scenario, which does not include this risk in its baseline scenario. Nevertheless, this is unlikely to change the ECB’s intention to raise deposit rates closer to 2% by the end of the year. The slowdown in European activity will be much more pronounced than in the US. The good news about Europe is that the union remains in place despite strong disagreements.

While no concrete decisions were reached at the European Council, the 27 member states did agree on a “roadmap” for implementing new measures in the coming weeks to combat rising energy prices. The EU member states want to reassure their unity and their willingness to provide a coordinated response to the energy crisis, which should help reduce the inflationary shock, limit the recession and support the euro. The European Council agreed to several proposals put forward earlier this week by the European Commission (grouped gas purchases for 15% of needs, creation of an LNG Europe index in addition to the TTF Europe reference for gas arriving by pipeline, a mechanism for correcting excessive prices, use of the €40 billion in cohesion funds to help the most vulnerable households and businesses). There is a great deal of uncertainty regarding supplies in the winter of 2023-2024. The catching up of gas storage continues in the countries that were behind. All of Europe except Latvia is now at a minimum of 80% of storage capacity. The level is much higher in France (99.4%) and Germany (96.5%). The start of winter remains mild and is also limiting short-term tensions and allowing more time for negotiations. On the political side, the Italian election did not have the same effect as in 2018. The willingness of the pro-Ukrainian and pro-European Prime Minister is reassuring (Giancarlo Giorgetti, a member of the moderate wing of the League, already Minister of Economic Development in Mario Draghi’s cabinet will take up the post of Finance Minister).

Sources : Bloomberg & Richelieu Gestion

MARKET REVIEW

A return to European Small Caps… maybe still a bit early

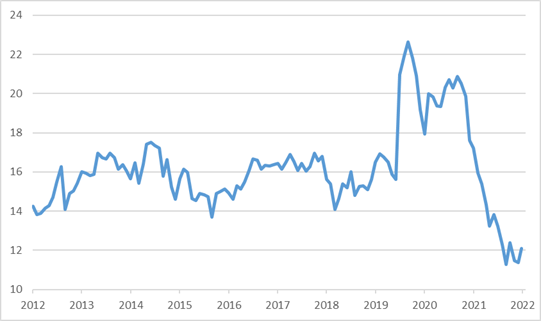

Since the beginning of the year, Small Caps are down 34% and have underperformed Large Caps by 20%, the worst performance since the 2000s. Valuations have become attractive given their growth profile. However, there are reasons for us to underweight the segment in the current market environment. SMIDs generally have greater domestic exposure (60% or more on average vs. 40% for the Stoxx 600) and are therefore less positively impacted by the rise in the dollar. They have lower profitability levels and margins may be more affected by inflationary pressures. Their bargaining power on prices remains more difficult. They generally offer higher levels of growth but are highly correlated to the economic cycle. They have little exposure to value sectors or to sectors that are currently outperforming (energy, banks) and are more sensitive to political/economic risks. Dividends (sources of stability for the investor) are lower. In addition, they suffer from a particularly large outflow since the beginning of the year. Their performance is closely correlated with M&A activity and consolidation deals, which are particularly sluggish at the moment due to rising rates. While we prefer to be cautious on the sector, we concede that at current levels (P/E of 12), many of the arguments mentioned above are already partly integrated. We favor a long position on quality SMEs (stable growth, balance sheet, good profitability) to the detriment of more indebted stocks that could still suffer from deteriorating credit conditions.

Sources : Bloomberg & Richelieu Gestion

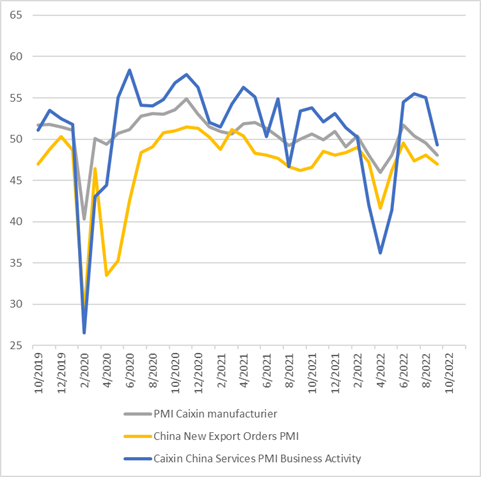

CHINA : astonishment and fear

The 20th Congress of the Chinese Communist Party was supposed to be one of the major events in modern Chinese history, not only because President Xi was expected to win a third term, which is rare, but also because it was taking place against the backdrop of the country’s slowest growth in decades. The “congress” effect did not take place. Unlike in the West, where negative market reactions can influence policy and even topple entire governments, it is becoming clear that investors are only a second-order consideration for Xi. This impression was reinforced by Beijing’s decision to delay the release of a series of economic data without explanation and further increase the doubts of investors who are already wary of Chinese assets. A reshuffle in Xi Jinping’s political party and yet more “Zero Covid” measures in China’s Guangzhou region are enough to worry.

Xi’s emphasis on loyalty over market-friendly leaders in promotions to the Politburo and its supreme standing committee represents a sea change in China. The 24-member Politburo is dominated by officials affiliated with Xi. It is also worth noting that the youngest new member of the standing committee, Ding Xuexiang, is 60 years old. This suggests that Xi has not designated a successor, who would traditionally be in his 50s to stay under the age limit before he can take office, and as such Xi Jinping may even seek a fourth term in 2027. The next appointments to the watch list will come in March 2023 and will be important for the markets. China’s sharp market decline on Oct. 24 highlighted Xi’s unchallenged grip on the ruling party. Tech giants Alibaba, Tencent and Meituan all fell as investors remained skeptical that Xi and his allies would change their attitude toward the private sector.

President Putin’s actions in Ukraine have drawn attention to China’s territorial ambitions. The Chinese president’s speech at the opening of the 20th Congress of the Communist Party in Beijing has raised many concerns. In particular, on the issue of Taiwan and the future of relations between China and the United States. The U.S. could implement new export controls to limit China’s access to some of the most advanced emerging computer technologies. Early discussions include quantum computing and artificial intelligence. Xi Jinping merely repeated the party’s antiphon that the “reunification” of Taiwan with the Chinese mainland under the party banner is inevitable and will be achieved by force if necessary. This is likely to add a significant risk premium to Chinese assets. This is why we are now negative on China, waiting for more clarity from the political leadership to the market.

Sources : Bloomberg & Richelieu Gestion

Bonds : volatility and profitability

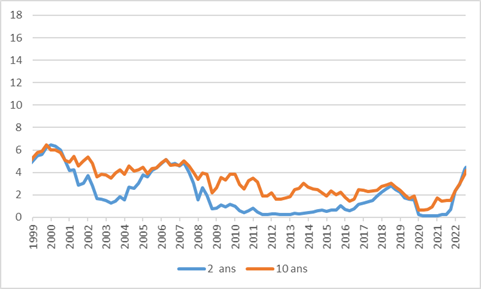

With 2-year Treasury yields around 4.60%, we believe we can begin to build up some of our short-term Treasury positions and continue to increase our positions if 2-year rates rise to the 4.80%-5.00% levels. We believe that the Fed terminal rate should not exceed the 4.75-5.00% level. The curve should remain inverted in the coming months. In terms of US 10-year rates, the 4.50% level should also be an entry point given the growth expectations for 2023. The challenge will lie in the continuation of monetary tightening and in the communication that J. Powell will adopt regarding potential future hikes of lesser magnitude, an element at the heart of our scenario and which should allow the long end of the yield curve to remain above 4.5% for a long time.

In corporate bonds, global IG yields are now above the level of high yield debt at the beginning of the year. We recognize that while we expect credit spreads to peak from IG EUR to B+140 bp, it is very difficult to have perfect timing, and once the market turns, we would not be surprised if spreads tightened quickly as investor appetite for profitability will increase once there is stronger visibility on inflation.

Sources : Bloomberg & Richelieu Gestion

UK : still have doubts about UK assets despite everything

Faced with the realization that she will not be able to implement the desired economic program and the resulting loss of credibility, the Prime Minister ended up resigning. This has fueled a new wave of easing on assets that had been battered by the spendthrift and unfunded “mini-budget”. If more cost-saving measures were to be introduced, the risk of moving to a policy of excessive austerity in a very weak economic environment would pose additional risks to British economic growth. R. Sunak had been much more cautious than Liz Truss on fiscal matters during the last campaign in August and had been very critical of the “mini-budget”, while the main challenge will be to restore fiscal credibility in the eyes of investors. For the Bank of England, the question of balance will arise, even if the priority will remain to fight inflation. The end of the Truss era should allow for a further reduction in thefears that weighed on British assets as well as those of the rest of the world, and in particular on European sovereign rates. Nevertheless, we remain cautious with regards to the GBP in the coming months due to the negative outlook for growth with the risk of a return to greater fiscal austerity and the Bank of England has not finished raising key rates to combat inflationary pressures and will therefore exacerbate its impact on activity.

Sources : Bloomberg & Richelieu Gestion

Synthesis of the Richelieu Group’s strategy – Author

Disclaimer

This document was produced by Richelieu Gestion, a management company subsidiary of the Compagnie Financière Richelieu. This document may be based in particular on public information. Although Richelieu Gestion makes every effort to use reliable and complete information, Richelieu Gestion does not guarantee in any way that the information presented in this document is.

The informations, opinions and all other information contained in this document are subject to change without notice. The information, opinions and estimates contained in this document are for information only. No element can be considered as investment advice or a recommendation, canvassing, solicitation, invitation or offer to sell or subscribe relating to the securities or financial instruments mentioned.

The information provided regarding the performance of a security or a financial instrument always refers to the past.

The past performance of securities or financial instruments is not a reliable indicator of their future performance.

All potential investors must carry out their own analysis of the legal, tax, accounting and regulatory aspects of each transaction, if necessary with the advice of their usual advisers, in order to be able to determine the benefits and risks of this transaction as well as its suitability, in view of its particular financial situation. He does not rely on Richelieu Gestion for this.

Finally, the content of research or analysis documents or their extracts possibly attached or cited may have been altered, modified or summarized. This document has not been prepared in accordance with regulatory provisions intended to promote the independence of financial analyzes. Richelieu Gestion is not subject to the ban on carrying out transactions in the securities or financial instruments mentioned in this document before its publication.

Market data is from Bloomberg sources.